![]()

Ureteral Stents Market to Surge from USD 711.8 Million in 2026 to USD 1,259.9 Million by 2035-By Rising Kidney Stone Prevalence, Biodegradable Stent Innovation

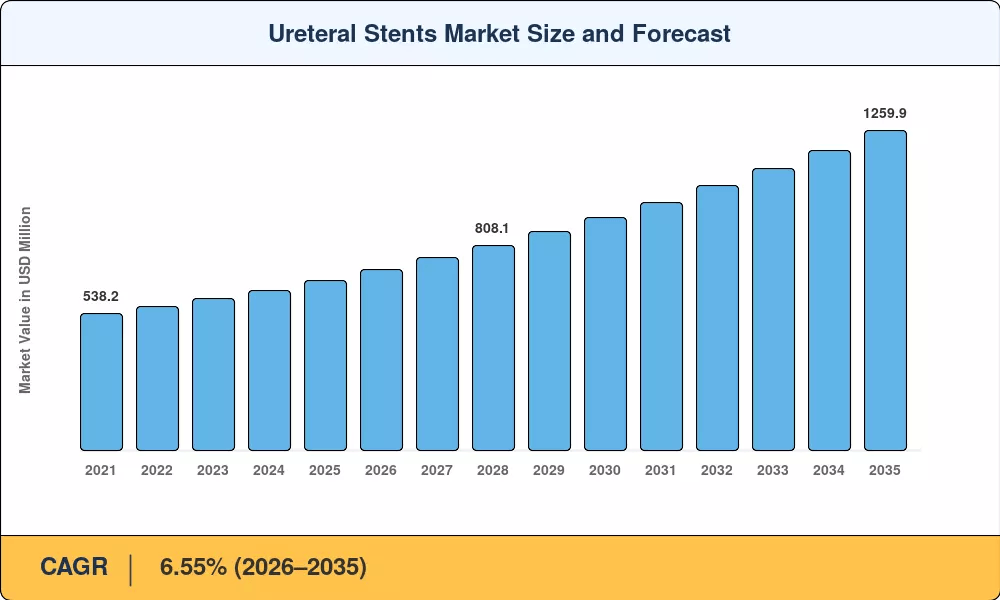

NY, CA, UNITED STATES, June 25, 2026 /EINPresswire.com/ — As per Market Research Future, the global Ureteral Stents Market size is projected to reach USD 1,259.9 Million by 2035 from USD 711.8 Million in 2026, at a CAGR of 6.55% during the forecast period 2026–2035. The market base was estimated at USD 668.0 Million in 2025.

The 6.55% CAGR—anchored by structural urology demand rather than discretionary healthcare spending—is driven by three converging forces: rising kidney stone prevalence that continues to widen the addressable patient base for minimally invasive drainage intervention, sustained biodegradable stent innovation that has pulled ureteral stenting from secondary removal dependency toward single-procedure protocols, and ambulatory surgical center migration that has converted ureteral stent placement from inpatient cost centers into outpatient reimbursement priorities tied to reduced chair time and throughput optimization.

Request A Free Sample:

https://www.marketresearchfuture.com/sample_request/1389

Key Market Trends & Growth Drivers

Rising Kidney Stone Prevalence and Extended Survival

Kidney stone incidence has climbed steadily across industrialized nations, with US prevalence reaching approximately 10% of the adult population according to recent urological survey data. The condition’s gender gap is narrowing—women under 60 now represent the fastest-growing patient cohort, increasing stent placement volumes in previously underserved demographics. Climate change and dietary shifts toward high-sodium processed foods compound this trend globally, with the WHO projecting a 25% increase in nephrolithiasis cases across South and Southeast Asia by 2030. Each diagnosis typically triggers at least one stent placement cycle, directly expanding the Ureteral Stents Market addressable base.

Biodegradable Stent Innovation

Legacy polyurethane and silicone stents still dominate operating theaters, but anti-encrustation nano-coatings and radiopaque biodegradable polymers are redefining performance benchmarks. A significant paradigm shift has occurred with the commercialization of bioresorbable polymers, which confirms the practical feasibility of temporary platforms designed to safely resorb within 4–8 weeks following surgery. Standard secondary removals include acute complication risks, such as ureteral perforation, and are projected to cost healthcare systems between USD 1,200 and USD 1,800 per event. By doing away with these follow-up steps, biodegradable designs are positioned as premium, high-margin products throughout the Ureteral Stents Market value chain, addressing both clinical safety and economic efficiency.

The U.S. FDA granted 510(k) clearance to the RELIEF biodegradable ureteral stent in January 2024, marking the first biodegradable design authorized for vesicoureteral reflux prevention. European Medicines Agency conditional approvals granted in recent years have shortened time-to-market for novel stent materials. The convergence of diagnostic imaging with biodegradable therapeutics is creating personalized urology platforms that tailor stent selection to individual patient metabolic profiles and anatomical requirements.

Ambulatory Surgical Center Migration and Value-Based Reimbursement

CMS expanded outpatient reimbursement codes for ureteral stent procedures in January 2025, enabling ambulatory surgical centers to perform a broader range of stenting interventions. ASCs offer 30–45% cost savings over hospital-based settings and reduce patient throughput times. North American ASC capacity grew 8.2% year-over-year in 2024, and similar models are expanding across urban India, China, and Brazil. This reimbursement-driven shift has converted ureteral stent placement from an inpatient cost center into an outpatient priority, with formulary committees prioritizing single-use kits and streamlined inventory programs.

Ask for Customization:

https://www.marketresearchfuture.com/ask_for_customize/1389

Market Segment Insights

BY PRODUCT TYPE

Double Pigtail Stents: Dominant segment with ~42.1% revenue share in 2025. Reflecting broad clinical versatility across stone management, transplant, and tumor indications. Their coiled retention mechanism provides reliable positioning across diverse anatomies, and decades of clinical experience make them the default choice for most urologists. Hospital procurement teams treat them as a default first-line agent, and established pricing has enabled broad adoption even in cost-sensitive emerging markets.

Biodegradable Stents: Fastest-growing product segment at 10.75% CAGR (2026–2035). Driven by clinician demand for the elimination of secondary removal procedures. Advances in poly(lactic-co-glycolic acid) and magnesium alloy composites are enabling controlled resorption timelines that match diverse clinical indications—from 3-week post-ureteroscopy drainage to 12-week tumor palliation.

BY MATERIAL

Polyurethane: Dominant material category, holding approximately 44.8% of segment revenue in the base year. Anchors institutional formularies globally due to its favorable balance of tensile strength, flexibility, and manufacturing cost. Hospital procurement teams treat it as a default first-line material, and competitive pricing has enabled broad adoption even in cost-sensitive emerging markets.

Silicone: USD 148.3 Million in 2025. Commands premium pricing in applications requiring extended indwell times, where superior biocompatibility reduces patient discomfort.

BY APPLICATION

Kidney Stones: Dominant application with ~56.8% revenue share in 2025. Correlating directly with escalating global nephrolithiasis incidence. Approximately 10% of US adults are affected, making stone management a near-universal component of urology care pathways. The inherent procedural frequency of stone disease drives sustained dual-channel demand for ureteral stenting.

Tumor-Related Obstruction: Fastest-growing application segment at 8.95% CAGR (2026–2035). Reflecting improved oncology survival rates that extend the window for palliative ureteral drainage. Immune checkpoint inhibitors and targeted therapies extending median overall survival create a larger prevalent population requiring sustained ureteral stenting.

BY END USER

Hospitals: Largest segment with ~63.0% share in 2025. Comprehensive urology service lines and complex case management dominate volume. Hospitals remain the primary delivery site for tumor-related obstructions, transplant patients, and pediatric cases due to specialized infrastructure requirements.

Ambulatory Surgical Centers: Fastest-growing end-user segment at 8.70% CAGR (2026–2035). Outpatient shift and cost optimization drive demand as single-use kits and streamlined inventory programs reduce the need for full surgical suites. ASCs and community urology clinics increasingly prescribe ureteral stenting to manage inpatient capacity.

Regional Outlook

North America — Dominant Market (~38.5% Share, 2025)

The United States generates approximately 72% of North American Ureteral Stents Market revenue, driven by high kidney stone prevalence, CMS outpatient reimbursement code expansions, and commercial insurance coverage of next-generation coated stents as first-line intervention—a single policy ecosystem that converted an inpatient-dominated market into one with a structural outpatient care tail. CMS coding updates in 2025 broadened outpatient stent procedure eligibility, accelerating the shift toward ASC-based care delivery. The US dominates through a combination of high per-patient spending, robust payer coverage, and rapid biodegradable adoption.

Europe — Second Largest (USD 181.7 Million, 2025)

Europe’s Ureteral Stents Market reflects divergent national strategies—Germany leads regionally with advanced urology infrastructure, contributing USD 47.2 Million in 2025, while the UK historically used selective stent targeting before broadening coverage through NHS pathway optimization. France contributes ~18.5% of regional share through hospital outpatient reform. Italy contributes on aging demographics. Spain is growing at steady pace on ambulatory procedure growth.

Asia-Pacific — Fastest-Growing Region (8.15% CAGR, 2026–2035)

Asia-Pacific is the engine of the Ureteral Stents Market. China holds the largest regional share with ~34% of regional revenue, driven by Healthy China 2030 hospital buildout—adding over 1,200 urology-equipped facilities between 2022 and 2025. India is growing at 9.10% CAGR on the back of Ayushman Bharat coverage expansion for over 500 million beneficiaries. Japan contributes USD 36.6 Million through geriatric urology demand at steady pace. South Korea is growing on advanced medical technology adoption.

Middle East & Africa — Emerging Opportunity (7.20% CAGR, 2026–2035)

The Middle East & Africa is bifurcated between well-funded Gulf states and resource-constrained Sub-Saharan nations. Saudi Arabia leads the region with Vision 2030 healthcare cluster development, contributing ~28% of regional share—NEOM health cluster and the UAE’s Cleveland Clinic and Mayo Clinic affiliations have created pockets of excellence for urological care. The UAE is growing on medical tourism for urological procedures. South Africa contributes on private hospital chain expansion.

South America — Growing Presence (USD 41.4 Million, 2025)

Brazil anchors South America’s Ureteral Stents Market at ~58% of regional revenue, with the Unified Health System (SUS) expanding urological procedure coverage in 2024, providing a stable demand floor that smooths regional forecasts. Access to advanced coated stents remains limited by import dependencies, though domestic production feasibility studies are underway. Argentina is growing at steady pace on private sector urology growth.

Competitive Landscape and Recent Developments

The Ureteral Stents Market exhibits medium concentration, with the top five companies holding an estimated 48–55% combined revenue share. The Herfindahl-Hirschman Index sits in the 800–1,200 range, reflecting a mix of multinational medtech conglomerates and specialized urology-focused firms. Strategic consolidation—exemplified by Teleflex’s EUR 760 Million acquisition of BIOTRONIK’s vascular intervention unit—signals that cross-selling synergies between vascular and urological product lines are reshaping competitive positioning.

The competitive landscape is stratified between coated stent innovation pioneers serving global urology markets, biodegradable platform expansion specialists capturing premium formulary listings, and single-use kit developers consolidating the ambulatory surgical center segment.

KEY COMPANIES AND RECENT MILESTONES

Boston Scientific Corporation (~12–16% share): Maintains leadership with Percuflex Plus and Contour platforms, commanding broad urology portfolio leadership. Global ureteral stenting leadership anchored by comprehensive product breadth across materials and indications.

Coloplast A/S (~9–13% share): Vortek and Polaris Ultra platforms reinforce the coated stent innovation positioning. Next-generation anti-encrustation coating line developed in partnership with a nanotechnology research institute, announced September 2023.

Cook Medical (~8–12% share): Resonance and C-Flex platforms reinforce the metallic stent specialist positioning. AI-assisted stent length selection tool integrated with Resonance metallic stent platform for ambulatory surgical centers, introduced November 2024.

Olympus Corporation (~7–10% share): HydroPlus and UroPass platforms reinforce the endoscopy integration positioning. Filed 510(k) premarket notification for a drug-eluting ureteral stent platform designed to reduce post-placement inflammation, February 2025.

Future Outlook: 2026–2035

By 2030, precision biodegradable stent theranostics will become the operating system of ureteral stent management. The convergence of companion diagnostics and targeted biodegradable therapy will reshape the Ureteral Stents Market through the late 2020s. By 2030, an estimated 40% of newly diagnosed kidney stone patients will undergo CT urography staging followed by matched stent selection, creating a diagnostic-therapeutic revenue loop. Machine-learning models that integrate metabolic, proteomic, and imaging biomarkers can recommend optimal stent material and dwell time for individual patients.

Biodegradable-driven access expansion and AI-integrated clinical decision support will reframe cost structures by the early 2030s. Regulatory clearances for next-generation biodegradable designs are accelerating product turnover cycles and reshaping how urologists approach post-procedural stent management.

More Related Research Insights:

https://www.marketresearchfuture.com/reports/urology-devices-market-1120

https://www.marketresearchfuture.com/reports/urinary-catheters-market-2538

https://www.marketresearchfuture.com/reports/kidney-stones-market-1745

https://www.marketresearchfuture.com/reports/minimally-invasive-surgery-devices-market-7875

https://www.marketresearchfuture.com/reports/nephrostomy-devices-market-32551

https://www.marketresearchfuture.com/reports/surgical-stents-market-1044

https://www.marketresearchfuture.com/reports/interventional-radiology-products-market-11546

https://www.marketresearchfuture.com/reports/surgical-equipment-market-556

https://www.marketresearchfuture.com/reports/urology-devices-market-1120

Larry Wilson

WantStats Research And Media Pvt. Ltd.

+1 855-661-4441

email us here

Visit us on social media:

LinkedIn

Facebook

YouTube

X

Legal Disclaimer:

EIN Presswire provides this news content “as is” without warranty of any kind. We do not accept any responsibility or liability

for the accuracy, content, images, videos, licenses, completeness, legality, or reliability of the information contained in this

article. If you have any complaints or copyright issues related to this article, kindly contact the author above.

![]()

Media gallery